Is The Best Go To Market Execution By An African Tech Company?

I'm just coming back from a research trip (holiday) to Dakar. In Dakar, you're never more than 1km away from the ocean, a cat, and a Wave mobile money agent. For a company so widely used and one that just raised a $200M Series A at a $1.7B valuation, it’s surprising how many people had never heard of them.

Wave was a spinout from Sendwave, which was acquired by Worldremit for $500M. Prior to the acquisition, I had never heard of them and I consider myself a pretty keen observer of the African technology ecosystem. Apparently, I wasn't the only one. According to PitchBook, only *one* African VC firm has invested in Sendwave/Wave. A Senegal based friend explained it to me like this:

These guys had piloted a bunch of ideas across Africa before coming to Senegal. They went outside of Dakar and rented a house to stay in with their core team in [a rural area] and quietly built Sendwave. They focused on customers outside of Dakar and were pretty under the radar. The only local VC that invested in Sendwave discovered them while doing due diligence for another company.

While scaling Sendwave, which was a remittances product, they realised that the user experience for local transfers could also be improved with the same product and distribution infrastructure they built for remittances. They began piloting the product that became Wave and ultimately spun it off after Sendwave was acquired.

Wave is the best example of what Wiza Jalakasi described as Mobile Money 2.0.

The first generation of mobile money companies was built by telcos for feature phones and on top of GSM infrastructure. Mobile Money 2.0 will be built by venture-backed companies for smartphones and on top of the internet.

In a telegram group that I’m a part of, there was a really insightful conversation by Moulaye Taboure and Bartel Latzoo on Wave which I’ve replicated here with light editing:

Wari’s (incumbent mobile money 1.0 operator) model and profits got destroyed by Wave over the last year. Wari was always the profitable (so more costly) alternative to Orange Money (another incumbent mobile money 1.0 operator), but in one year Wave exceeded both of them due to a great product, low fees, and aggressive marketing.

Orange Money and Wari have really poor products and notoriously bad customer support. Wari only launched their mobile app recently while being the oldest of the three.

Wave is primarily available as a smartphone app. The app uses very little data, so is accessible for users that cannot afford 3G/4G subscriptions. For users without smartphones, they can access it through QR cards, which can be used just like Visa cards. The user experience is vastly superior to the alternatives which require clicking through multichoice USSD menus.

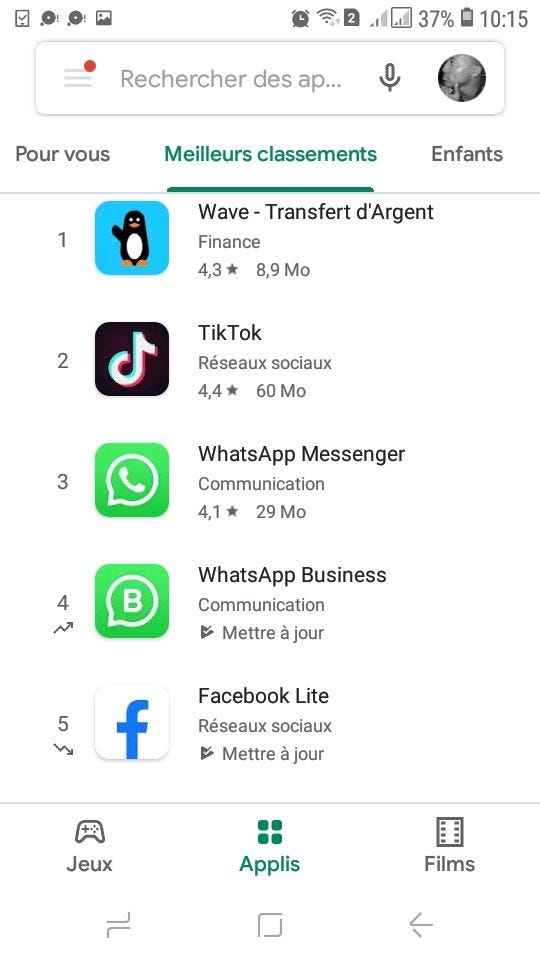

Wave doesn’t just provide a better service, it does so at a lower cost. 0% deposit fees. 0% cash-out fees. 0% fees for bills payment. 1% for transfer fees. Mobile money customers in Senegal realized that Orange Money was milking their pockets with higher fees and mostly switched to Wave. The results were immediate. Wave is now the most downloaded android app in Senegal. More downloaded than FB, TikTok, and WhatsApp.

[My comment: There was a similar situation in India, where UPI and competition completely decimated fee revenues for mobile payments operators. Ultimately, if you want to make sustainable revenues in digital payments, you have to do more than just help people send and receive money].

Honestly from the ground here in Ivory Coast, the execution was admirable (those blue penguins are all over the place and more visible than Orange or MTN by far). They started by canvassing the interior of the country [my comments: the same approach they used with Sendwave in Senegal]. When they entered the capital, their agent network visibility was supported by great content on social. I saw a dozen different TikToks or comedy skits welcoming the ‘'Blue Penguin’ against the ‘evil corporations’.

If you want to dig a little further, I’ve curated a short reading list of articles to help you understand the history of mobile money and what its evolution could look like:

M-Pesa and the African Fintech Revolution by Marc Rubenstein (link)

The Fight for Mobile Money 2.0 by Wiza Jalakasi (link)

Wave - Building a Cashless Africa by Everett Randle (link)

Fintech in LatAm: Banking the Unbanked by Aika Ussenova (link)

Digitizing the mom-and-pop store

Jeff Bezos famously said “Your margin is my opportunity” while Jim Barksdale said “there are only two ways to make money on the internet, bundling and unbundling”.

These two quotes, more than any other, describe how technology entrepreneurs attack sectors ripe for disruption. Entrepreneurs are always looking for large bundles with healthy margins that can be unbundled into more focused products that are tailored to the user’s specific needs.

In the early ‘00s, Craigslist was the target. Entrepreneurs would pick a section on Craigslist, and build it into a vertically focused marketplace. Companies such as AirBnB, Reddit, Tinder, Indeed, Zillow, and Upwork emerged from this wave.

Image credit: Andrew Parker

Next fintech came for the banks. Bank functions like payments, savings, lending, and cross-border transactions were all targeted by challengers building products focused on just one specific function.

Image Credit: CBinsights

Today, entrepreneurs in emerging markets are attacking the informal retail sector. As is often the case in these markets, there is nothing to disrupt and so the sector is instead being made more efficient.

Retail in emerging markets is largely dominated by informal mom-and-pop stores. These stores are largely operated with pen and paper, cash, and mobile phones. Mom-and-pop stores are not being disrupted in the same way banks and Craigslist were disrupted in the previous examples. What we’re seeing instead is entrepreneurs focusing on digitizing all their core process:

While the chart above from this excellent article (link) focuses just on India, this trend is happening across all emerging markets.

Inventory procurement (e.g. TradeDepot and Chiper)

Book-keeping (e.g. Trienta and Shara)

Digital payments (e.g. Yoco and Clip)

Digital store front (e.g. Brimore, Nuvemshop and oList)

Remember, the only ways to make money are bundling and unbundling. None of these players is really content to just focus on one process. The goal is to bundle all the processes into a single platform and become the ‘OS for mom-and-pop stores’ as a recent fundraising announcement put it. Each product wants to become the primary platform that mom-and-pop stores use to execute all their key processes.

The other key thing to remember is that ‘margin is opportunity’ but there is finite margin to be captured from making mom-and-pop stores more efficient. This is why every player wants to expand into financial services particularly lending.

It’s still pretty early days in this trend and there are a few things we don’t yet know the answer to. Which process would prove to be the most effective wedge to becoming the ‘OS of mom-and-pop stores’? Which are the strategic moats that would allow them to scale embedded finance into a major revenue driver?

I’m writing a deep-dive on digitising the mom-and-pop store, online markerplaces/platforms, and embedded finance. If you want to speak, send me an email.

Play to Earn

There’s a common joke on Twitter that we haven’t gotten any new episodes of Black Mirror because we’ve been living in one for the past 18 months.

In a story straight from Charlie Booker’s notebook, young Filipinos, unable to work during the pandemic, are applying for loans in order to buy Axies, which are basically video game characters that you can use to earn Smooth Love Potions in a game called Axie Infinity. Because this is 2021, each Axie is an NFT, and you can trade your Smooth Love Potions for cryptocurrencies like Ethereum, which can then be converted to cash.

You need three Axies to start playing Axie Infinity. Over a year ago, Axies cost as little as $4-$5. Today, they can go for upwards of $500. Roughly half of Axie Infinity’s over 1M players are based in the Philippines. The majority of them cannot afford $1500 to start playing the game so they look for ‘sponsors’ who can provide them with ‘scholarships’ in return for their earnings from the game or they can rent pay a portion of their earnings as interest.

a16z is just invested $4.6M in tokens owned by Yield Guide Games (YGG), a Philippines-based company that owns a ton of Axies and manages 4700 scholars. YGG’s business model is to discover games similar to Axie Infinity (games where there is a land-based economy with native tokens). YGG then acquires some tokens. As the value of these tokens increases, YGG will sell them or rent them out to players who want to play to game but cannot afford tokens.

These “play-to-earn” games are being framed as a source of economic mobility and an opportunity for young people, particularly in developing countries, to make money. I’m very skeptical. First, we’re in the middle of a crypto bull run, and a lot of the activity on these platforms is driven by speculation. Even if these platforms outlast this current bubble, the owners of platforms (such as Axie Infinity) and the providers of capital (such as YGG) will capture most of the value. Competition is likely to drive down profits for the average player to the barest minimum.

If you want to dig a little further, I’ve curated a short reading list of articles about play to earn games:

A deep dive on free to play games by Ryan Foo (link)

If you're reading this and you have any experience with play to earn, I would love to chat.

Interesting Links

ARK invest podcast with Chipper Cash founder Ham Serunjogi. Chipper Cash is executing a very aggressive growth strategy for an African fintech, but it’s clear from this interview that Ham understands how large the opportunity is and that he needs a lot of resources to tackle it. In a way, Chipper Cash is doing to cross-border payments what Wave is doing to mobile money (link)

Apparently trying to replicate Indian payment products in Mexico doesn’t work because of fraud and a lack of trust [I’m generally skeptical about explanations like this when given by someone who isn’t from the region] (link)

Every new technology is an opportunity for Africa to leapfrog, apparently, this time its BNPL (link)

Witty letter to the editor at FT suggesting that developing countries need to leapfrog leapfrogging (link)

Interview on VC in emerging markets with Mikal Khoso, who is really smart on these topics (link)

Twenty minute VC has recently done 3 great podcasts focused on LatAm with a16z’s Angela Strange (link), Kaszek’s Nico Szekazy (link), and SoftBank’s Marcelo Claure (link)

Great overview presentation on the South East Asia fintech space (link)

Article in the Verge about Netflix’s big push into Nollywood. Summary: results are mixed so far (link)

Article on the competitive dynamics of banks and consumer fintechs in Pakistan. It sounds a lot like the Nigerian fintech space (link)

| Y Combinator's Work at a Startup")

Wonderful piece