Unevenly Distributed

Personal Updates. Softbank in LatAm. Africa is the last region standing. YC's batch size.

Some life updates.

It’s been almost a year since I last sent out an edition of this newsletter. A lot has happened in that time. I moved to a new city in a new country (if you’re based in the Bay Area and want to grab a coffee, say hi!). I also joined FirstCheck Africa & Ralicap as a Venture Partner (if you’re building a pre-seed or seed stage company in Africa or Latin America, say hi!). I’ve also settled into a new role at Endeavor - focused on helping our entrepreneurs find the right capital partners.

Some newsletter updates.

It’s been hard to put out this newsletter while settling into a new country and juggling multiple new commitments. I have about 3 unpublished articles in my drafts that I’ve started and just haven’t been able to take to completion.

I’ve decided to experiment with a new format for the newsletter. I’ll be modeling it very closely after Benedict Evan’s and Matt Levine’s newsletters. Meaning I’ll mostly do a mix commentary and curation on the most important news in technology.

I’ll still focus on emerging markets. Mostly Sub-Saharan Africa, MENA, LATAM, and Asia. I don’t know what the publishing schedule will be, but hopefull I can get something out once a month. I’ll still put out longer pieces whenever I have a topic to explore and my schedule permits it.

There are a handful of other changes coming to the newsletter in the next few weeks/months. Stay tuned.

On to the newsletter.

A new era for Softbank in Latin America

There’s a really nice article in protocol that explores the rise of the VC ecosystem in Latin America. It heavily quotes a handful of investors including former Softbank Managing Partner, Shu Nyatta. It also pretty extensively features the Softbank Latin America fund - arguably the most important investor in the region over the past few years.

In the 5 years from 2014-2018, Latin America received $4.7B in venture capital funding. Then in March of 2019, Softbank announced a $5B fund focused entirely on the region. A month later, it would announce a $1B investment into just one company - Rappi. In 2021, Softbank would announce a plan to commit a further $3B to Latin America. Given the amount of interest in Latin America today, it’s easy to forget how big of a deal the Softbank Latin America fund (then called the Innovation Fund for Latin America) was at the time. Softbank bet big on Latin America before many other investors and it paid off. When the fund launched in 2019, there were only 9 unicorns in Latin America. Softbank’s LatAm portfolio today contains 32 unicorns. The company has invested $7B into the region over 3 years and generated a very respectable 32% blended IRR.

Softbank’s Latin America fund was led by Marcelo Claure together with Managing Partners Shu Nyatta and Paulo Passoni. All three of them have recently left the firm. According to LinkedIn, Marcelo is currently running his family office, Shu has started a firm called Bicycle, and Paulo is on ‘gardening leave’. The LatAm Funds, which used to be run separately, will now be rolled into the Vision Fund family. It feels very much like the end of an era. However, the LatAm ecosystem today is much more robust than when LatAm fund was announced in 2019 and Softbank deserves a lot of credit for that.

Funding slump across markets - except Africa.

In my job, I spend a lot of time talking to investors who are active or looking to get active in emerging markets. Last year, there was a palpable level of interest and excitement in these markets. I felt this in almost every conversation. The numbers bear this out, with record levels of fundraising across most emerging markets.

Half of the investors I spoke with said “I’ve made money in LatAm, so I’m getting more active there and looking to become active in other emerging markets”. The other half of investors went “I missed out on LatAm so I’m looking to become active there and starting to explore other emerging markets”.

I started to classify funds into three categories:

Active: These funds have pools of capital and partner-level resources dedicated to a particular region.

Opportunistic: These are the funds that may have made a handful of investments but do not yet have resources dedicated to a particular region. They typically have a very high bar for investing in the region and would only make an investment under certain circumstances. For example, if it comes highly recommended from a trusted source or it fits very neatly into their thesis.

Exploratory: These are the funds that are still largely learning about a region, trying to decide whether to dedicate more time and capital to it. They are taking meetings and maybe even visiting the region but they have not yet made an investment. I like to say that they’ve brought their notebooks to the region but they haven’t yet brought their checkbooks.

In the past quarter, it seems every VC firm has gone down a level when it comes to emerging markets. The previously active firms are now opportunistic, the opportunistic firms are now exploratory, and the exploratory firms are now firmly focused on their core markets.

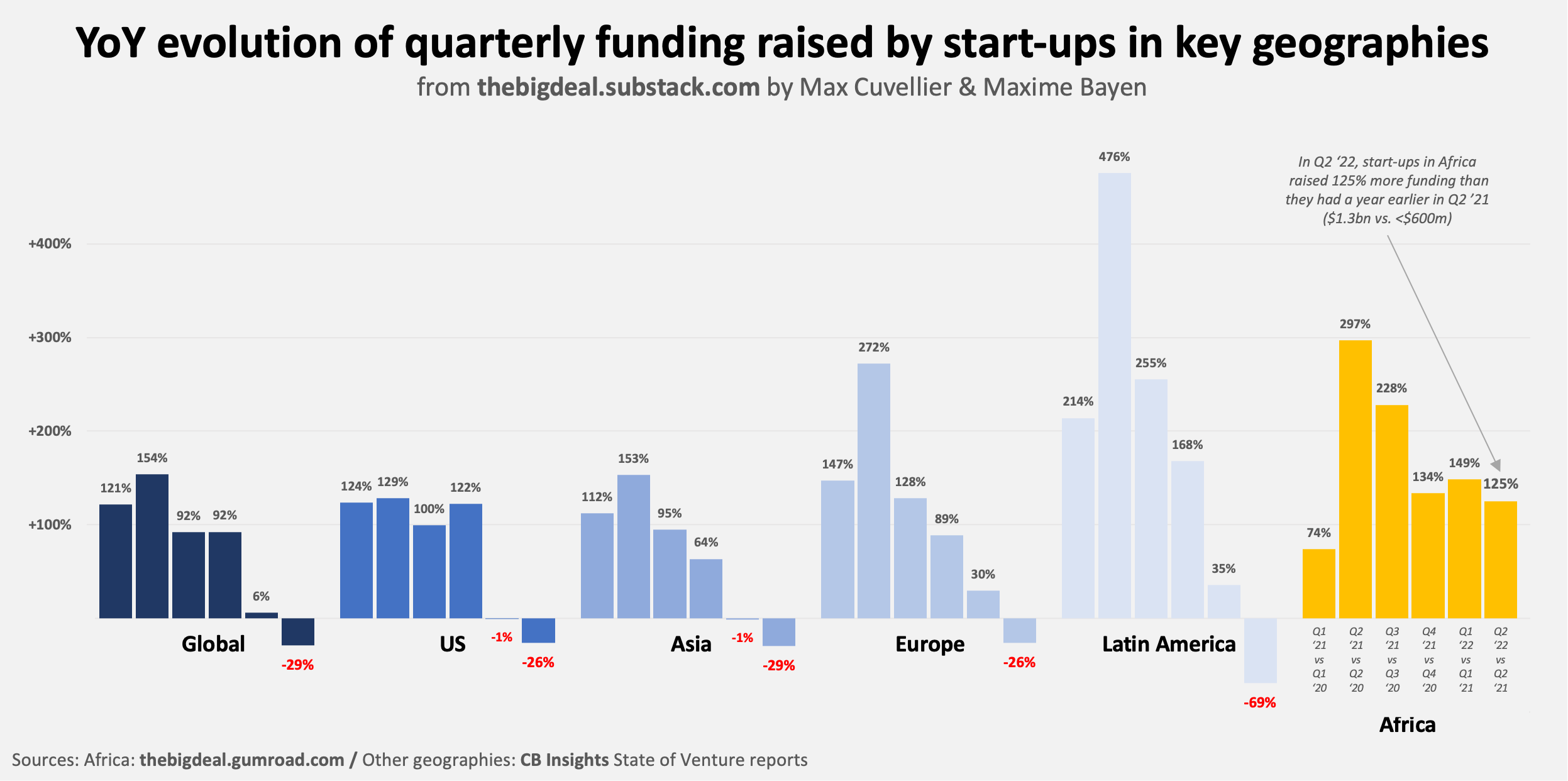

Again the numbers bear this out. Globally, VC funding dropped by ~25% from a quarter ago and from Q2 last year. In LatAm, VC funding was down ~66% from Q2 last year. In Asia, VC funding dropped ~20% from Q1 2022 and Q2 2021. However, in Africa, the numbers were up pretty significantly.

This is from Maxime Bayen and Max Cuvilliere:

Yet, the story the numbers tell us is pretty solid. Start-ups in Africa have raised $1.3bn in Q2 2022, which adds up to $3.1bn in the first half of the year. Let me put it this way: June 2022 was the ecosystem’s strongest June ever in terms of fundraising. Q2 2022 was the ecosystem’s strongest Q2 ever. H1 2022 was the ecosystem’s strongest H1 ever. And we’re not talking small increments here; we’re talking 2.7x, 2.3x and 2.4x year-on-year growth, respectively.

There are three reasons why I think the Africa numbers have not yet slowed down, even though anecdotally, I’ve seen interest in the region slow down. All of them are related to the fact that the global slowdown in fundraising has mostly been at the later stages.

First, growth stage funding in Nigeria has started to trend down like other regions. However, because the growth stage market in Nigeria never represented as large a portion of total fundraising as it does in other markets, then the effects of this drop are not as much.

Second, Africa’s growth stage market is still highly concentrated. Only five companies are responsible for 40% of the $4.6B of growth stage capital raised in Africa since 2019. In any given quarter, if one or two of these companies raise rounds then it’s enough to keep the numbers from going down meaningully. However, this means that total capital raised at the growth stage can vary pretty wildly from quarter to quarter.

Third, Africa has a longer deal lag than other regions. Deals tend to take pretty long to get closed, particulary at the growth stage. This means that many of the deals that have been announced this year were probably set in motion since last year, before the decline in public market prices.

However, my prediction is that we will see a meaningful drop in the numbers for Africa in the second half of the year both sequentially and year on year. Given the current y-o-y growth from last year, African start-ups are on track to raise ~$8B this year, I suspect the final numbers will be closer to $5B-$6B.

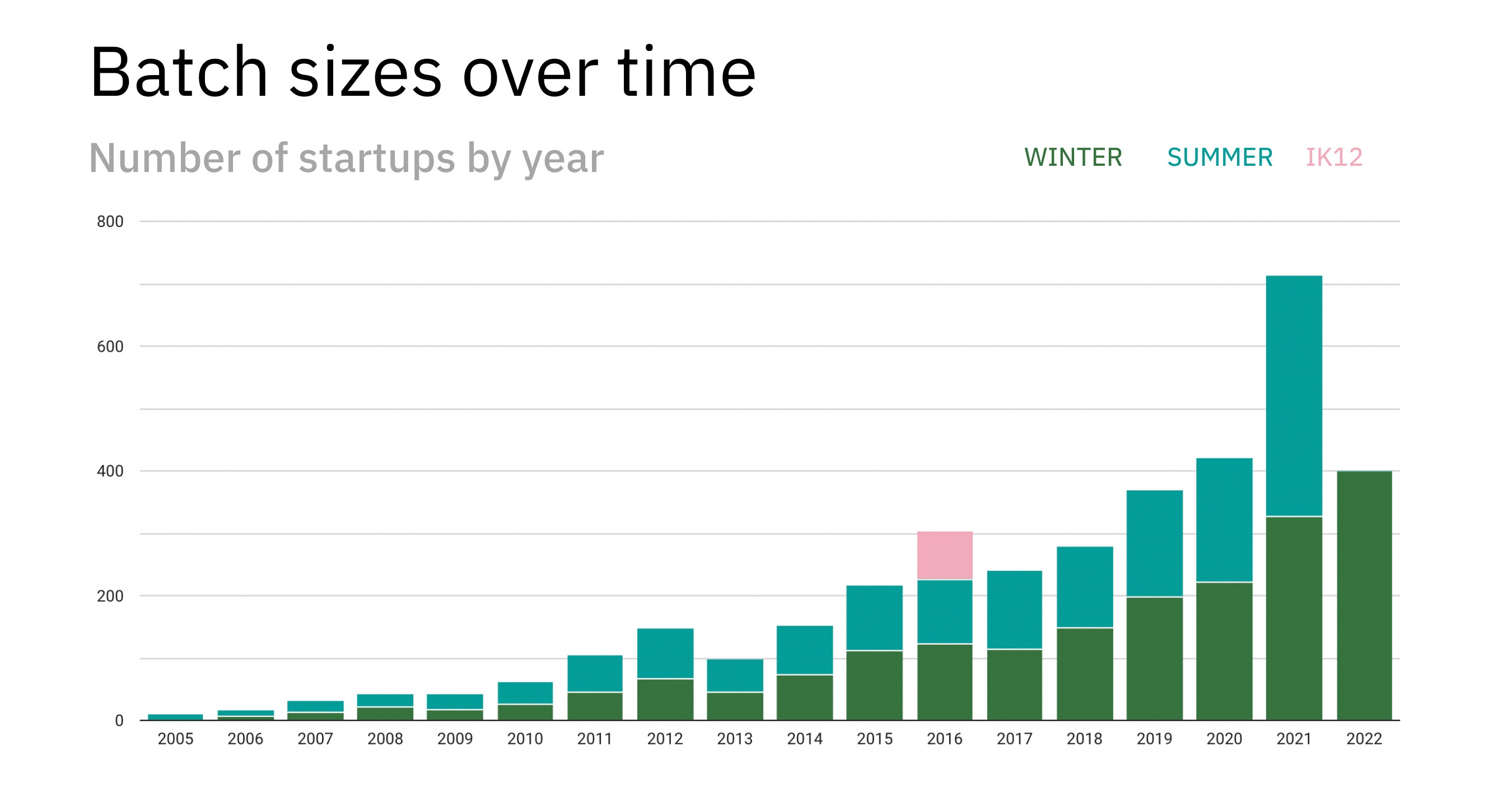

Y-combinator’s road to a 1,000 company batch hits a speed bump

The Information reported that Y-combinator will be slashing its batch size by 40% due to macroeconomic conditions and the “realities of being back in person”. The new YC batch will have about 250 companies. This is a marked change from YC’s tone last December when president Geoff Ralston mused about someday having a 1,000 company batch. As recently as this March, Geoff wrote this blog post about scaling YC.

YC has grown its batch consistently since it launched 16 years ago. The first YC batch was eight companies. The twentieth batch had hundred companies. Four years later, the batch size had doubled to two hundred companies. It doubled again within eighteen months.

As Paul Graham said in the thread below, at almost every stage of that journey, YC has gotten criticized for growing too fast.

The push back to YC’s increasing scale is centered around two arguments: that scale dilutes YC’s brand and degrades the experience for founders. The latter might have some merit but the former not only misses the mark, but has it exactly backward.

It’s difficult to argue that the founders in an eight-company batch and founders in a four-hundred-company batch can receive the same quality of attention. In 2012, the first time YC reduced its batch size, Paul Graham alluded to this

The reason we accepted fewer applications was that in summer 2012 we grew too fast. We had 66 companies in winter 2012, and that was fine, but for some reason more things than usual broke when we jumped from 66 to 84.

However, PG also stated that YC didn’t intended to keep the batch size small

We don't plan to stay at 50, or whatever exact number of startups this batch ends up having… We've been tweaking our model, like we always do, and we hope some of the tweaks will push the limit back.

Today, YC thinks it has figured out how to continue scaling while maintaining the quality of the founder experience. Here’s a tweet from PG making that case:

Geoff Ralston echoed the same sentiment in the interview where he speculated about a 1000 company batch.

“If we want to fund 1,000 companies a batch, could we?” Ralston wondered aloud in a Zoom chat with me the other day. “Well, yeah. If we can hire another 10 or more folks — who have the same passion for startups that we do and want to spend a lot of time reading applications and working with startups and and creating those transformative experiences.”

I don’t know how well this strategy works but I do think that it is imperative for YC to continue to grow its batches if it wants to maintain its brand. It’s a mistake to think that YC’s brand comes from its exclusivity. It comes from the quality of its batches and more importantly from the success of its big winners such as Stripe, Coinbase, Doordash, and Airbnb.

Investors will continue to come to demo day as long as the quality of startups in YC’s batches is higher than most other sources of deal flow. This will be continue to be true if YC the best companies continue to apply to YC and YC has a good filter. As batche sizes have grown, YC has maintained its acceptance rate at >3%. The growth has come from a growth in the number of applications it receives. That growth, in turn, has come from a growth in the startup ecosystem. There are simply more startups being started today than there were 16 years ago.

If YC maintained a batch size of say 50 companies while the start-up ecosystem grew, it might have remained more exclusive but it would have drastically increased its chances of eventually becoming irrelevant.

At a batch size of 50 companies today, there’s no level of filtering or no bar high enough that would guarantee it would be a batch of 50 Airbnbs. Instead, YC would have just increased its chances of missing the next Airbnb, Stripe, or Coinbase. Meanwhile, any generational company that YC misses is an opportunity for a competitor to build its own reputation.

I think it’s inevitable that as the global startup ecosystem grows and more competition emerges, YC will become less central and influential. However, remaining small only speeds up that process. The best way to maintain it’s position for as long as possible is for YC to keep growing and no one knows the importance of growth more than Y-combinator.

Thrilled to see you're back writing here again. Cheers.