UD #04: Nigeria's Mobile Money Moment

MTN, TeamApt, Paga, and Opay walk into a bar

In ‘The Chicken or The Exit’ co-authored with Osarumen Osamuyi, I wrote this:

However, even the most optimistic estimates would put Africa firmly in the experimentation stage or the beginnings of the scaling stage. The continent only just had its first unicorn. China had its first unicorn in 2010, and it took five years for it to get to five unicorns; the year after that, it had twenty. Ecosystems develop very slowly, and then all at once.

When I wrote this earlier in the year, Africa had one unicorn - Interswitch1. Today, we have 3 unicorns, with Flutterwave and Opay joining the stables2.

I was recently a guest on the Africa Tech Round Up podcast’s Unajua series where I tried to answer the question ‘Is the African technology ecosystem at an inflection point?’ (spoiler alert: it is).

In the first episode, embedded below, I talk about how looking at the number of unicorns always undersold the opportunity for digital financial services in Africa. There are four billion-dollar financial services businesses in Africa hidden inside telcos. MTN MoMo, Airtel Money, Mpesa, and Orange Money all generate between $1B-$400M in yearly revenues. Even the most conservative multiple would value all of them at more than $1B.

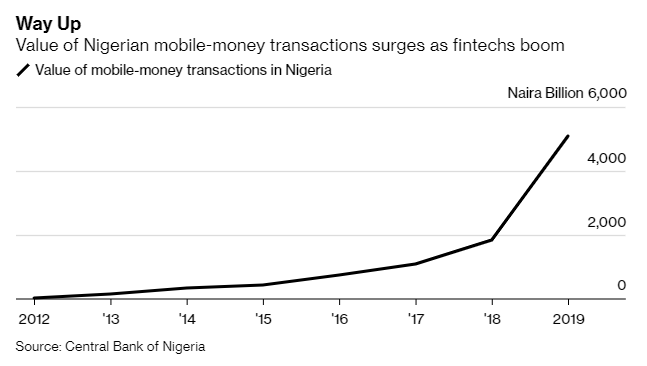

The mobile money revolution that has taken over the continent has largely skipped Nigeria. This has primarily been due to regulatory and market structure reasons which I won’t go through in this post (mostly because I don’t completely understand it myself, lol).

The relative failure of mobile money to take hold in Nigeria has left the country lagging behind other African countries in financial inclusion levels. Bank penetration is not as high as in South Africa or Namibia. While mobile money penetration is not as high as in places like Kenya or Tanzania. This leaves Nigeria stuck in the middle of nowhere, with ~50% of the country excluded from formal financial services.

This is starting to change. The CBN finally granted telcos the license to independently operate in financial services about a year ago. Banks are increasingly investing in their agency networks. Pure play agency banking players are also experiencing rapid growth. Opay processed $2B in transaction volumes last December. Paga processed ₦1T over the past 15 months, after processing ₦2T in its first ~7 years. TeamApt processed ~$4B in transactions in 2020, growing its agent network 9x. The number of financial services agents operating in Nigeria grew 5x in 2019. During last year’s lockdown period in Nigeria, when bank branches were not available, agent transactions grew by 859% between March and April 2020.

The potential for emerging markets to ‘leapfrog’ or at least catch up to the developed market in financial services has been much talked about. But in Nigeria, there’s still a multi-billion dollar opportunity in merely catching up to its peers.

Take MTN, for example. The company's financial services operations in Nigeria have historically been limited by regulation and the need to partner with a bank as it did not have a license to hold customer funds. Today, it has a super-agent license that allows it to hold funds and it has started to invest heavily in growing out its agent network. To give a sense of the potential for growth, MTN generated $112M in fintech revenue in Nigeria in 2020. It generated $212M in mobile money revenues from Ghana in the same year. Ghana’s GDP is less than 15% of Nigeria’s and MTN Nigeria has more than 3x the number of subscribers of MTN Ghana.

Mobile Money in Africa is entering its second phase, expertly captured by Wiza Jalakasi in this brilliant article. At the same time, the continent’s sleeping giant, Nigeria, is finally having its mobile money moment.

Rally Cap Asia is live, with a focus on Bangladesh, Pakistan, and Indonesia; to learn more, you can check out our deck or reach out to hayden@rallycapventures.com.

Rally Cap is building a global ETF of early-stage emerging market fintech, and they’re excited their portfolio has expanded to include:

Asia

Africa

LatAm

Other

Jumia is a public company, so it’s not a unicorn, even though it’s valued at over $1B. It’s the same reason why Fawry doesn’t count.

The Chipper Cash CEO never explicitly confirmed its billion-dollar valuation so I’m choosing to exclude it from this list.

Hi Derin, there's a CB insights unicorn overview that shows Chipper cash has a $1.5B valuation. https://www.cbinsights.com/research-unicorn-companies?utm_source=CB+Insights+Newsletter&utm_campaign=129647b61f-newsletter_general_Thurs_20210603&utm_medium=email&utm_term=0_9dc0513989-129647b61f-95627614

Hi Derin, there's a CB insights unicorn overview that shows Chipper cash has a $1.5B valuation. https://www.cbinsights.com/research-unicorn-companies?utm_source=CB+Insights+Newsletter&utm_campaign=129647b61f-newsletter_general_Thurs_20210603&utm_medium=email&utm_term=0_9dc0513989-129647b61f-95627614